JUSTICE FOR BARBARA KAY CRAWFORD

AUDIO RECORDING OF FRANK L. WILSON STATING HE WOULD KILL OR HAVE BARBARA’S SON KILLEDCLICK BELOW TO LISTEN

12/09/2025

CONVERSATION WITH JEFF FORTENBERRY, Union County GA. CORONER, and SON of JOAN FORTENBERRY

HOW DID WILSON’S EMPLOYEE -JOAN FORTENBERRY, BARBARA CRAWFORD’S CAREGIVER GET POSSESSION OF BARBARA’S REMAINS AND DEATH CERTIFICATE 1 YEAR BEFORE ATTORNEY JEREMY MOESER REQUESTED THE SAME FROM WILSON FOR HER CHILDREN?CLICK BELOW TO LISTEN

12/08/2025

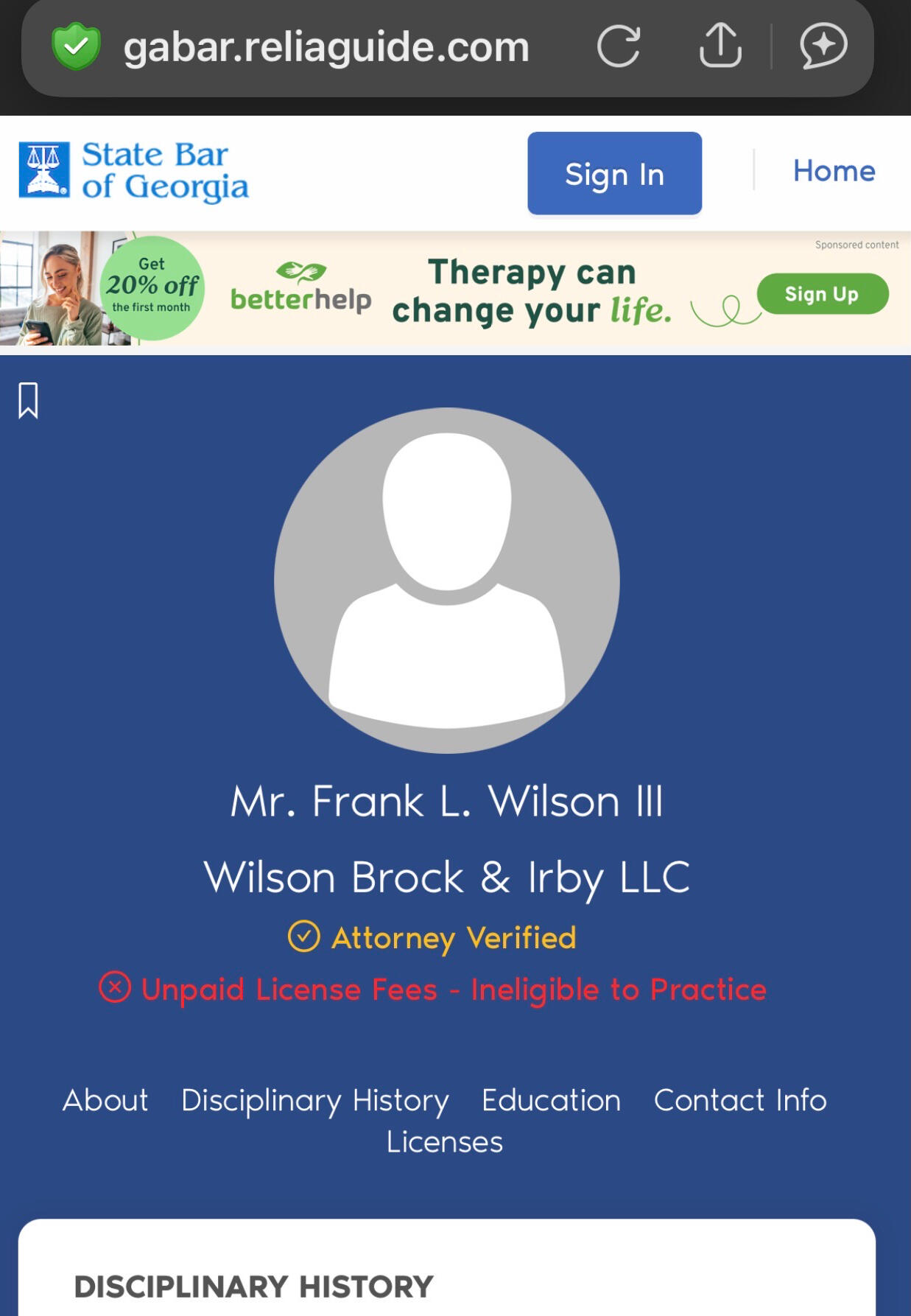

Conversation with Wilson’s secretary, Nan Ritchie Philpot

12/06/2025

FBI follow up

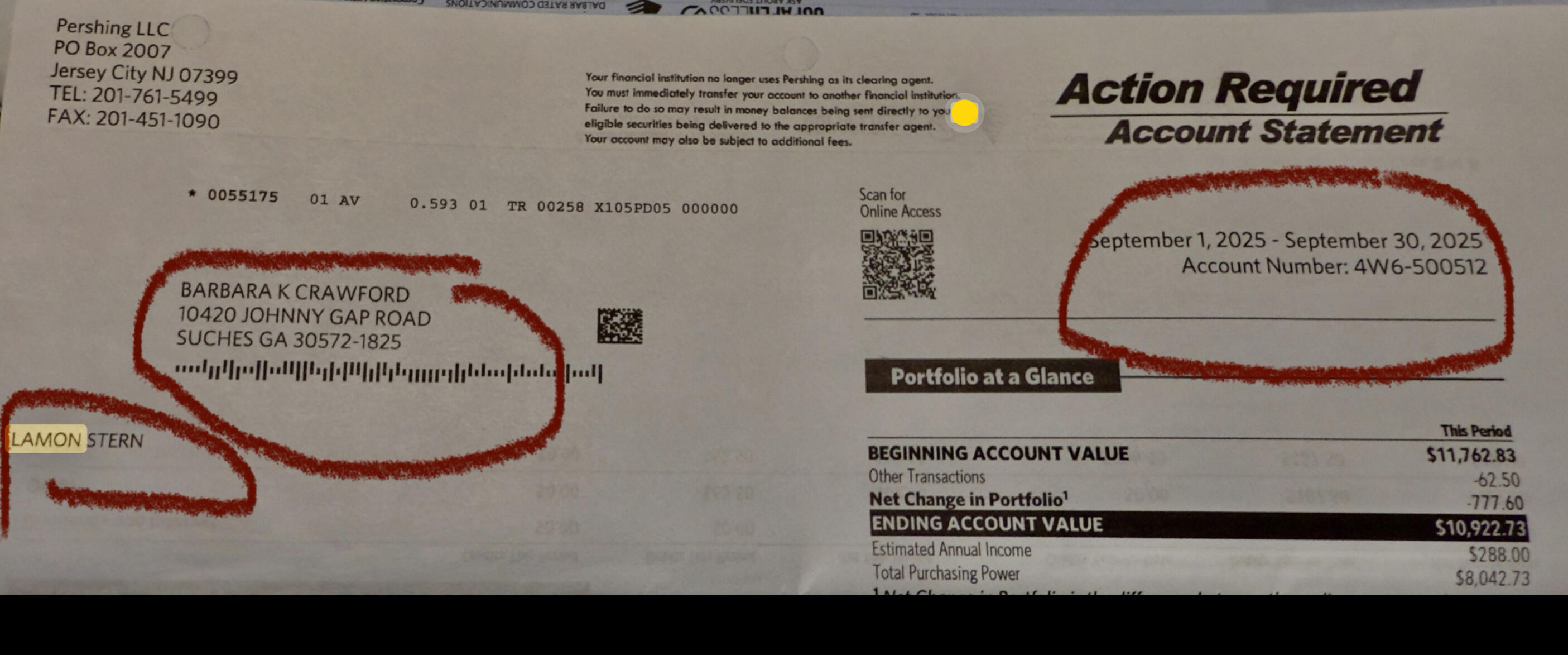

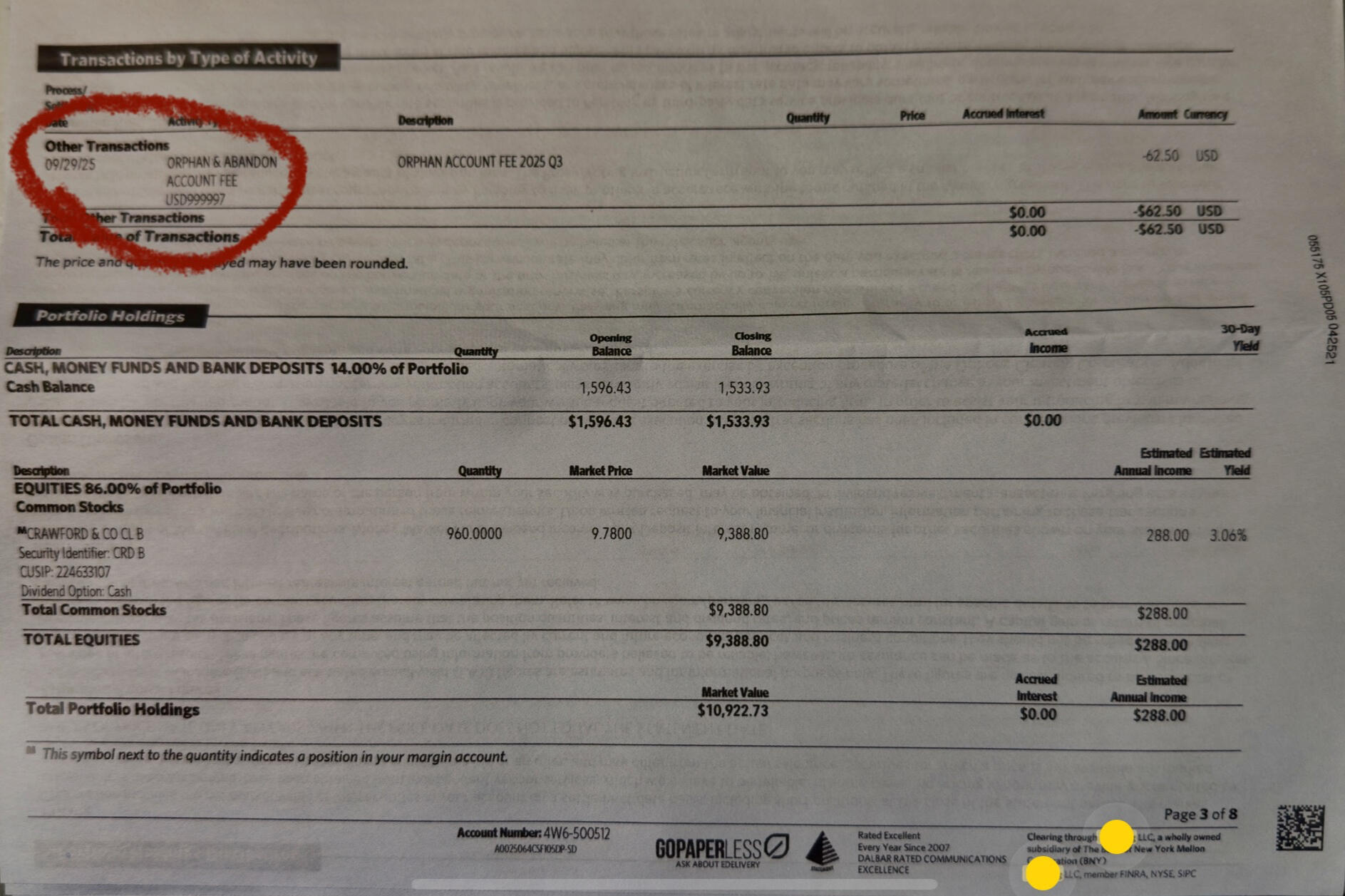

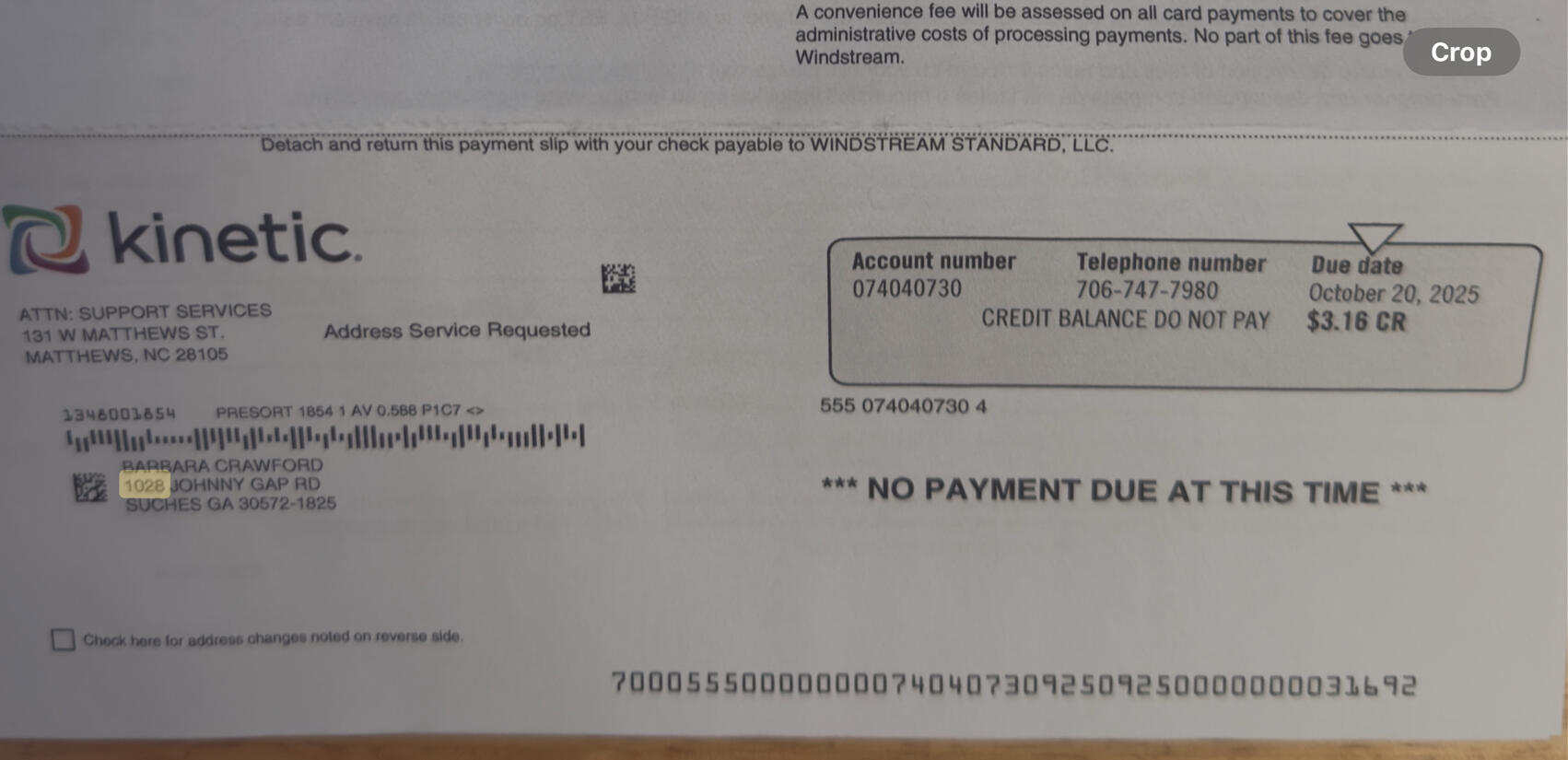

Why is Barbara still receiving Pershing statements and utility bills one year after her death?

$30,000,000 Family trust?

Maybe somebody should ask Frank Wilson or Hollis Lamon, right?

CODED TRUST DISBURSEMENTS TO BARBARA FROM FRANK L . WILSON III FOR ILLICIT SUBSTANCES.

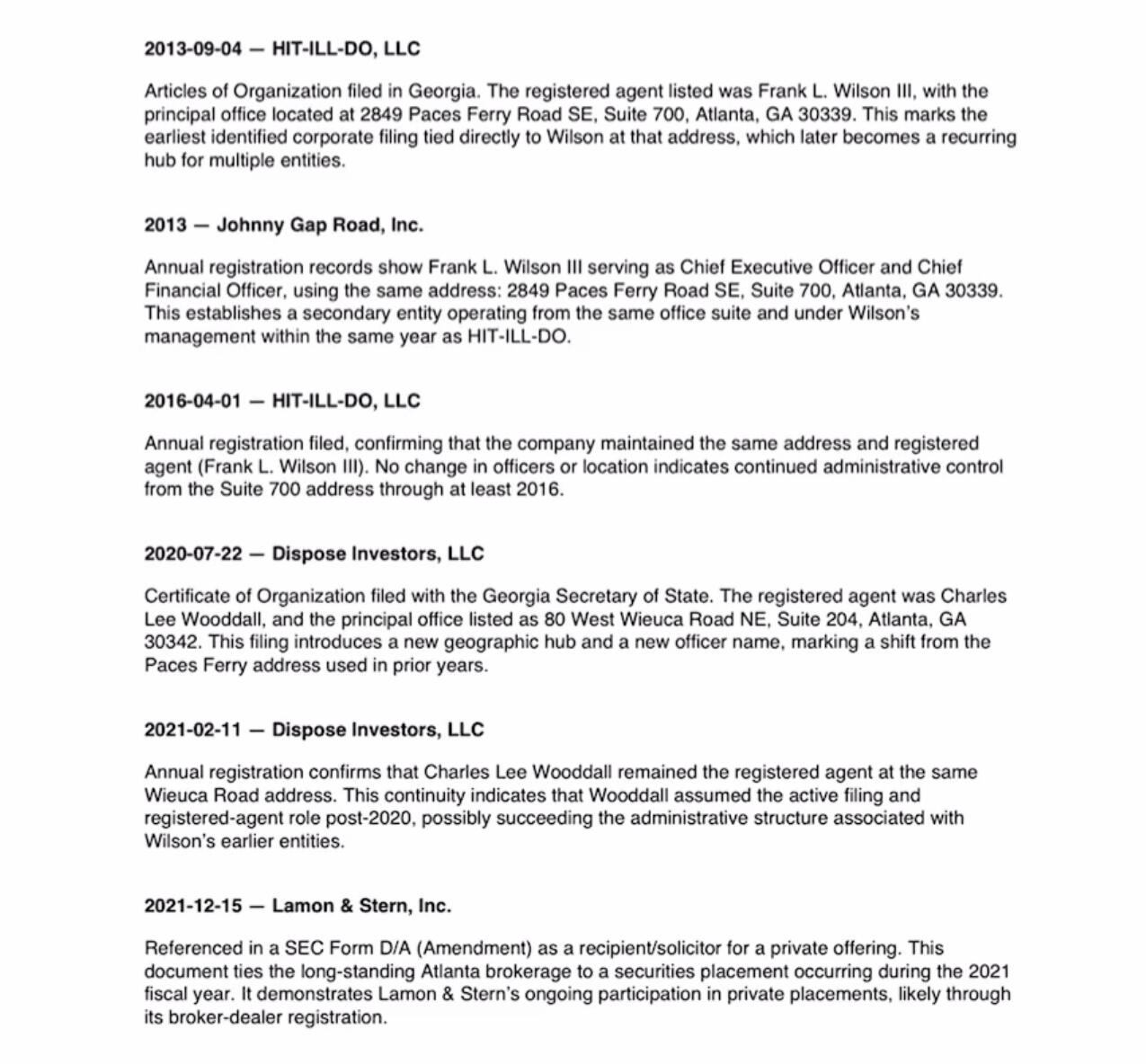

HIT-ILL-DO LLC?

DISPOSEINVESTORS LLC?

SERIOUSLY?